The Significance of Land Value Taxation

and Land Speculation

Julian Hickok

[Reprint of a booklet containing two papers, written

by Julian Hickok, founder and former Director of the Philadelphia

Extension of the Henry George School of Social Science. 1969]

FROM THE EARLY DAYS of the movement there has been some

misunderstanding-in the public mind as to the significance of the

reform advocated by Henry George.

"Progress and Poverty", by Henry George, begins as: "An

Inquiry into the Cause of Industrial Depressions and Increase of Want

with Increase of Wealth." In Book VIII, Chapter II, he writes: "What

I, therefore, propose, as the simple yet sovereign remedy, which will

raise wages … afford free scope to human powers … and carry

civilization to yet nobler heights, is -- to appropriate rent by

taxation." Continuing, he writes: "For rent being taken by

the State in taxes … every member of the community would

participate in the advantages of its ownership … as we abolish

other taxes, we may put the proposition into practical form by

proposing -- "To abolish all taxation save that on land values."

From this latter statement the remedy proposed by Henry George became

known as the "Single Tax".

As early as 1911 political activity was being conducted in New York

City under the name of "Single Tax". By 1920 the Party

Attained national significance with nominees on the ballot in a number

of states for President and Vice President of the United States. The

results of this campaign, however, were discouraging. Analysis of the

situation was made by prominent leaders and conclusions were drawn by

some that the weakness of the movement was in the name "Single

Tax."

Opposition to the name "Single Tax" was based upon the

contention that the remedy was not taxation but the collection of rent

for public benefit. A number of schemes were proposed for the

collection of rent without taxation. So strong was the objection to

use of "Single Tax" that the name of the Party was changed

to "Commonwealth Land" at the National Convention in New

York in 1924. A Platform was drafted, based upon the collection of

rent rather than upon the taxation of land values. Nominees for

President and Vice President were again placed upon the ballot in the

several states. The results were again discouragingly small. By this

time Oscar H. Geiger, who had been a member of the National Committee,

concluded that political activity should give way to popular education

in the fundamentals of economics, as expounded by Henry George. Soon

thereafter he founded the Henry George School of Social Science. From

this, together with the shift in emphasis from collection of rent to

land value taxation, the movement has made much progress.

In "Progress and Poverty," in advance of the statement of

his proposition, Henry George writes: "Nor to take rent for

public use is it necessary that the State should bother with the

letting of lands, and assume chances of favoritism, collusion, and

corruption this might involve. It is not necessary that any new

machinery should be created. ...We already take some rent by taxation.

We have only to make some changes in the modes of taxation to take it

all."

In shifting emphasis from taxation to rent, the argument was advanced

that taxation of land values was self-defeating in that the market

price of land would fall with increase of tax rate, ultimately

eliminating the base upon which the tax would be levied. A more

careful study of this phenomenon, however, should prove the fallacy of

the argument. The conclusions should be reached that: "As the tax

rate is increased and approaches infinity as a limit, land value

(price) decreases and approaches zero as a limit, and tax revenue

increases, approaching the full economic rent as a limit." From

this, no matter how high the tax rate, there would always; be some

base upon which to levy, and tax revenue would increase with increase

in tax rates. At no rate could tax revenue exceed the full economic

rent.

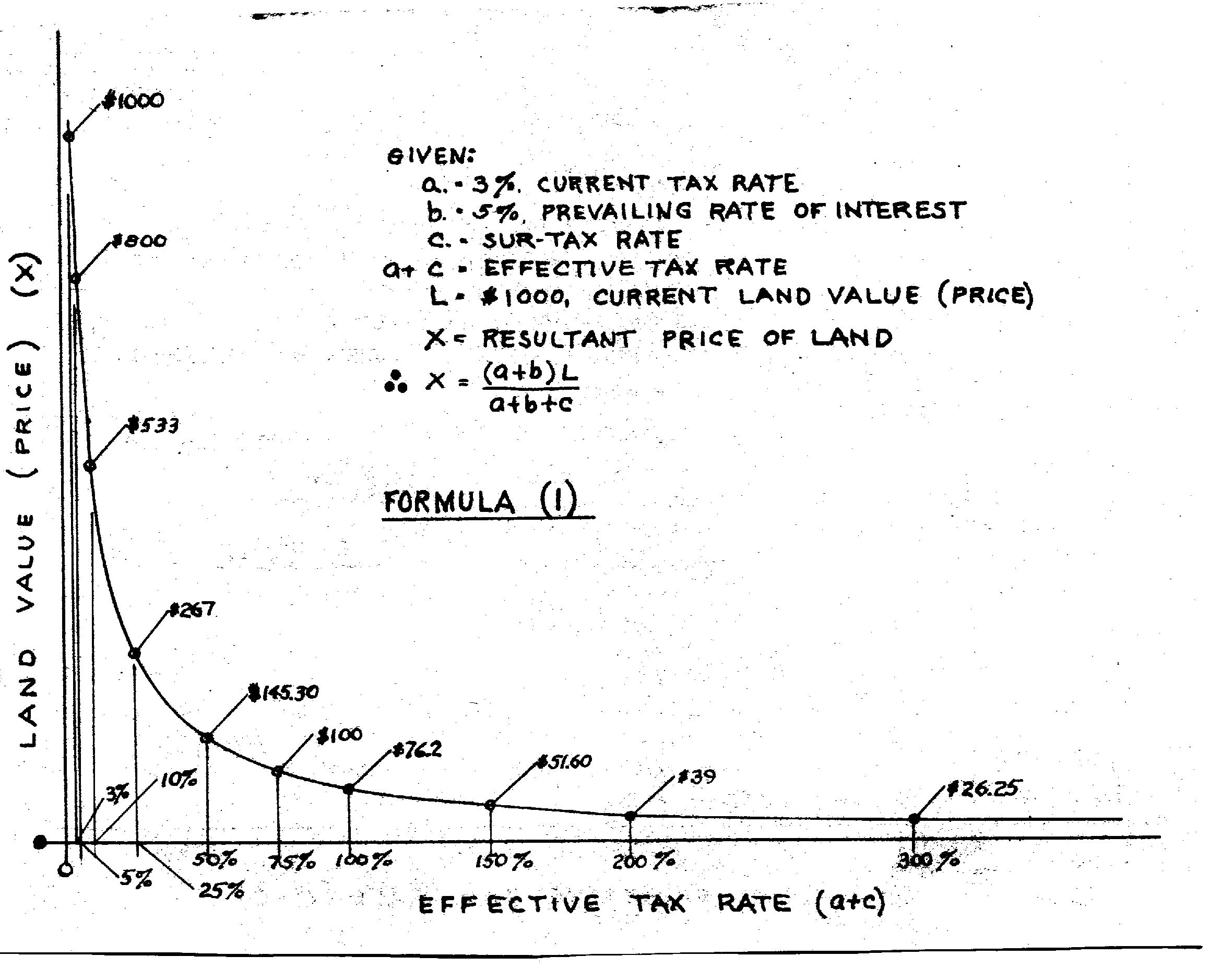

Chart I.

To demonstrate the above statements we may set up an algebraic

equation based upon the Law of Rent. Rent is a monopoly price, "all

that the traffic will bear." It is a fixed amount at any given

instance and is comprised of taxes, interest, and any other charges

that may be against the land. (See Appendix). The market price of

land, popularly known as, and herein referred to as Land Value, is the

capitalization of that part of rent assured to the owner. "

On these premises,

- let R = annual rent of land

- let a = current rate of

taxation, %

- let b = prevailing rate of

interest, %

- let L = Land Value (price)

- then R = (a + b)

L

- let c = increase in rate of

taxation, % points

- and X = resultant Land Value

(price)

- then R = (a + b + c) X

- from which X = (a + b)L / a + b

+ c

Formula 1

LAND VALUE (PRICE) RELATIVE TAX RATE

Using nominal values for a and b, as 3% and 5% respectively, and

solving for X in Formula 1, for various rates of taxation (a + c), we

may construct a graph to show the ratio of X to tax rates. There will

be a rapid decrease in X for small initial increases in tax fates,

following nearly a straight line until at a 20% effective tax rate,

where the value of X would be at about 30% of the initial Land Value.

Then the line would curve sharply to where at a 50% tax rate, X would

be at about 15% of the initial Land Value. At a 100% tax rate, X would

be at about 7%% of initial Land Value. At a 200% tax rate, X would be

at about 4%, and so on until at a tax rate of infinity, which is

impracticable, X would be at zero.

CHART II

For further study of this phenomenon, we may set up another algebraic

equation for tax revenue, (T):

Let T = (a + c)X

Formula 1a

From this we may construct a graph to show the amount of tax revenue

for the various rates of taxation (a + c), using X as derived from

Formula 1. Tax revenue (T) will approach the full economic rent at an

infinite tax rate. For the same nominal values used above for a and b,

tax revenue (T) will increase rapidly for small initial increases in

tax rates, following nearly a straight line until at a 20% effective

tax rate, T would be at about 80% of the rent. The line would

then curve sharply to where at a 50% tax rate, T would be at about 90%

of rent. At 100% tax rate, T would be at about 95% of rent. At 200%

tax rate, T would be at about 97-1/2% and so on to infinity at which

the maximum of 100% of rent would be taken.

Practical consideration in application of Formulae 1 and la would

lead to the conclusion that a gradual approach should be taken with

initially small increments of increase in tax rates over a

comparatively long period of time. Sufficient notice should be given

of all proposed tax rates to allow for market adjustments and to avoid

undue "jar or shock" to the economy. In fact it would be

practically impossible to get popular support for any drastic approach

to the ultimate application of the remedy.

TAX REVENUE RELATIVE RENT

As an appeal for acceptance of Land Value Taxation, it may well be

offered as an alternative for introduction of new taxes or increases

in taxation of other sources of public revenue, such as incomes,

sales, etc. It can readily be demonstrated that for a given increase

in public revenue, an increase in tax rate on Land Values would be far

less of a burden on the rank and file of commerce, industry, and labor

than the imposition of other forms of taxation. Furthermore, another

practical consideration of the application of Land Value Taxation

would be the limitation of the ultimate tax rate to about 100%. From

Formula 1, this would be at about 7-1/2% of the initial Land Value and

would be an incentive to greater investment of capital in commerce and

industry upon the land.

In words of Henry George, immediately preceding his proposal to

appropriate rent by taxation, "By leaving to land owners a

percentage of rent which would probably be much less than the cost and

loss involved in attempting to rent lands through State agency, we

may, without jar or shock, assert the common right to land by taking

rent for public uses." Since the levy of 100% tax rate would

provide about 95% of rent for public use, there would be left about 5%

of rent to private appropriation as compensation for administration. A

pragmatic approach to the ultimate tax rate should be made gradually

to determine the lowest percentage of rent to be left to induce proper

administration of land ownership while providing the maximum

appropriation of rent for public benefit.

Further consideration should be given to the statement by Henry

George: "We may put the proposition into practical form by

proposing to abolish all taxation save that on land values." This

would presume upon the ultimate removal of all taxes on such sources

as incomes, sales, etc., as well as upon buildings and other

improvements in or upon the land. Advocates of Land Value Taxation

usually present a program for comparable reduction or complete

elimination of taxes on improvements along with increase in tax rates

on land values.

An analysis of the Law of Rent as applicable to investments in real

estate should be made. The term "real estate" includes land,

which is a factor of monopoly, and improvements, which is a factor of

competition. A tax on land tends to decrease the market price while a

tax on improvements tends to increase the market price. The tax on

land can not be shifted by the land owner. The tax on improvements

must be borne by the tenant, who may or may not be the land owner. The

tax on improvements may be reflected in reduction of maintenance and

in curtailment of construction, which would continue until the market

is sufficient to reverse the trend.

In Formulae 1 and la we considered tax rates on land only. For a

differential in rates on land and improvements, by decreasing the tax

rate, or granting a rate of exemption on improvements, the yield for

investments in real estate tends to become correspondingly greater.

Thus there would be a compensating factor in a simultaneous increase

in the tax rate on land value with a rate of exemption on

improvements. The net result would depend upon the ratio of tax

exemption to tax increase and the ratio of values of the respective

bases upon which the rates would apply. If within a given area in

which the rates are to be adjusted, the total of land values is equal

to the total of improvement values, and the two rates were the same in

amount, there would be no reduction in land values nor any increase in

tax revenue. This would hold up to the point where the rate of

exemption is equal to the initial tax rate. Further decrease in the

tax rate on improvements would be negative and in effect a subsidy to

the land owner. Such is not to be considered in this analysis. For

complete exemption of improvements from taxation, with land values

equal to improvement values, and with a tax rate on land greater than

double the initial tax rate, land values would decrease and tax

revenue would increase.

If the ratio of total land values to total improvement values is

other than unity but equal to the ratio of rate of exemption to tax on

land values, there would be no decrease in land values nor any

increase in tax revenue. If, however, the ratio of land values to

improvement values is greater than the rate of exemption to tax on

land, there would be a decrease in land values and an increase in tax

revenue; conversely, land values would increase and tax revenue

decrease.

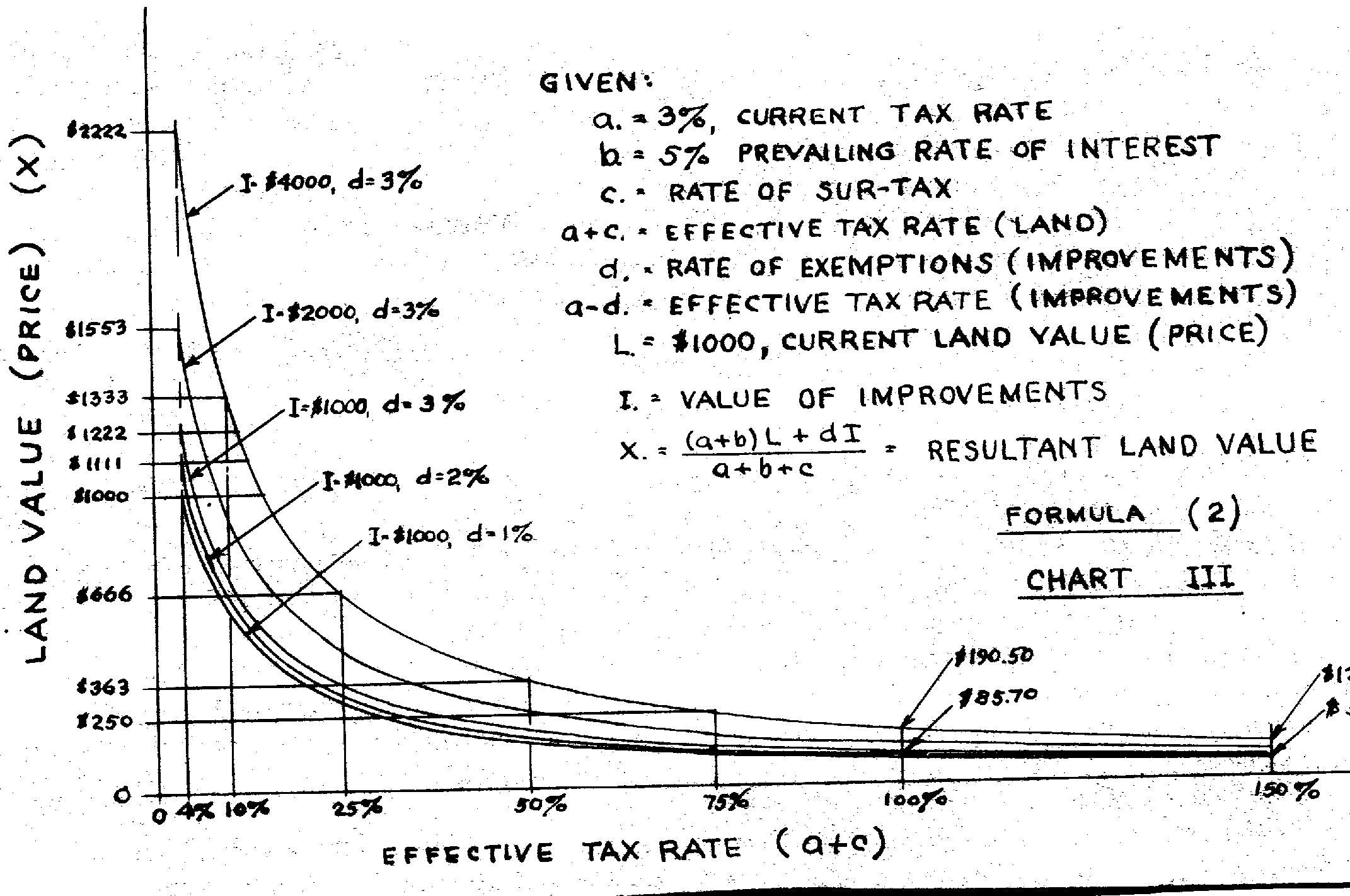

CHART III

To demonstrate the above statements, we may set up an algebraic

equation based upon the fundamentals of real estate investments - land

and improvements. The market price of land is the capitalization of

that part of the yield which is assured to the owner out of the rent

on land and sufficient to attract investment in the whole property.

On this premise,

- Let Y = yield, annual return on investment

- Let a - current rate of taxation, %

- Let b = prevailing rate of interest, %

- Let L = Land Value (price)

- Let I = Improvement Value

- then Y = (a + b)L + (a + b)I

- Let c = increase in rate of taxation, %

- Let d = decrease in rate of taxation, %

- Let x = resultant Land Value (price)

- then Y = (a + b + c)X + (a + b)I

- from which X = (a + b)L+dI / a + b + c

Formula 2

It may be noted here that if there is no exemption of improvements;

or d equals zero, Formula 2 is identical with Formula 1. With the

introduction of factor d, it is necessary to consider the relation of

all the factors; c, d, L and I. Using one factor only, d or I, as the

variable for each series of computations and solving for X, we may

construct graphs to show the relation of X to various tax rates and

property values. There should be several graphs, but all will follow

the pattern of graphs constructed from Formula 1.

It will be shown that when L/I = d/c, Land Values will be stabilized.

If L/I is less than d/c, Land Values will be increased; conversely, if

L/I is greater than d/c, Land Values will be decreased.

LAND VALUE (PRICE) RELATIVE TAX RATES AND EXEMPTIONS

CHART IV

Having determined the resultant land value, X, for various rates of

taxation and relation of values, we may determine the resultant tax

revenue for the various rates and values. For this we set up another

algebraic equation for tax revenue, T:

T = (a + c) X + (a - d) I

Formula 2a

from which to construct graphs to show the relation of tax revenue,

T, to various rates of taxation and values. Using X as derived from

Formula 2, it will be shown that the several graphs follow the same

pattern as in those derived from Formula la. As Land Values, X,

decrease, tax revenue, T, increases and vice versa.

TAX REVENUE RELATIVE YIELD

For Land And Improvements

CONCLUSION

Taxation of land values, derived from the capitalization of that part

of rent assured to the land owners is the most efficient, practical

and safe mode of taking rent for public benefit. It avoids the danger

of any levy upon land holdings in excess of rent, and respects the

rights of private property. It takes as much of the rent for public

benefit as practicable and in the shortest possible time with popular

consent.

Land Value Taxation with the elimination of other modes of taxation

and provision against subsidies or privilege to land owners would, in

the words of Henry George, "...raise wages, increase the earnings

of capital, extirpate pauperism, abolish poverty, give remunerative

employment to whoever wishes it, afford free scope to human powers,

lessen crime, elevate morals, and taste, and intelligence, purify

government and carry civilization to yet nobler heights."

APPENDIX

By definition, rent may include charges upon land other than taxes

and interest. It may be designated as (G) for "ground rent"

or its equivalent, from which we may set up an equation for Rent:

- R = (a + b) L + G

- then Formula 1 becomes:

X = (a + b) L + G / a + b + c

- and Formula 2 becomes:

X = (a + b)L + dI + G / a + b + c

In the use of these formulae it should be noted that the factors a,

b, c and d are percentage points while G is an amount so that the

percentages do not cancel out unless G is multiplied by 100. For

simplicity or brevity in this analysis, the use of "ground rent"

or equivalent charges, is neglected but the patterns of graphs for X

and T will be the same as when derived from formulae 1, la, 2 and 2a.

Land Speculation - Boom and Bust

In substance as presented at the Henry George School Conference

in St. Louis, Missouri, 23 July, 1966

For many years the world of business, finance and industry has been

stimulated, from time to time, with increased wages, prices and

profits,, associated with land prices, only to be depressed by an

economic decline. This phenonenon is well illustrated on a "Chart

Showing Land Price Swings in Chicago, 1830 to 1956", which is

contained in an article on "LAND" in the August 1960 issue

of "House and Home". On this chart, land prices are shown as

rising at relatively fixed nominal rates of increase over relatively

long periods of time followed by rapidly rising land prices and,

subsequently, by rapidly falling land prices, over relatively short

periods of time.

These cycles do not cover fixed intervals of time but do show that

rapid rises in land prices are always followed by rapid declines with

inevitable depressions. This is the picture of "Boom and Bust".

An analysis of the influence of speculation on land prices should show

the cause of spectacular rises in prices and lead to the remedy for

effective control.

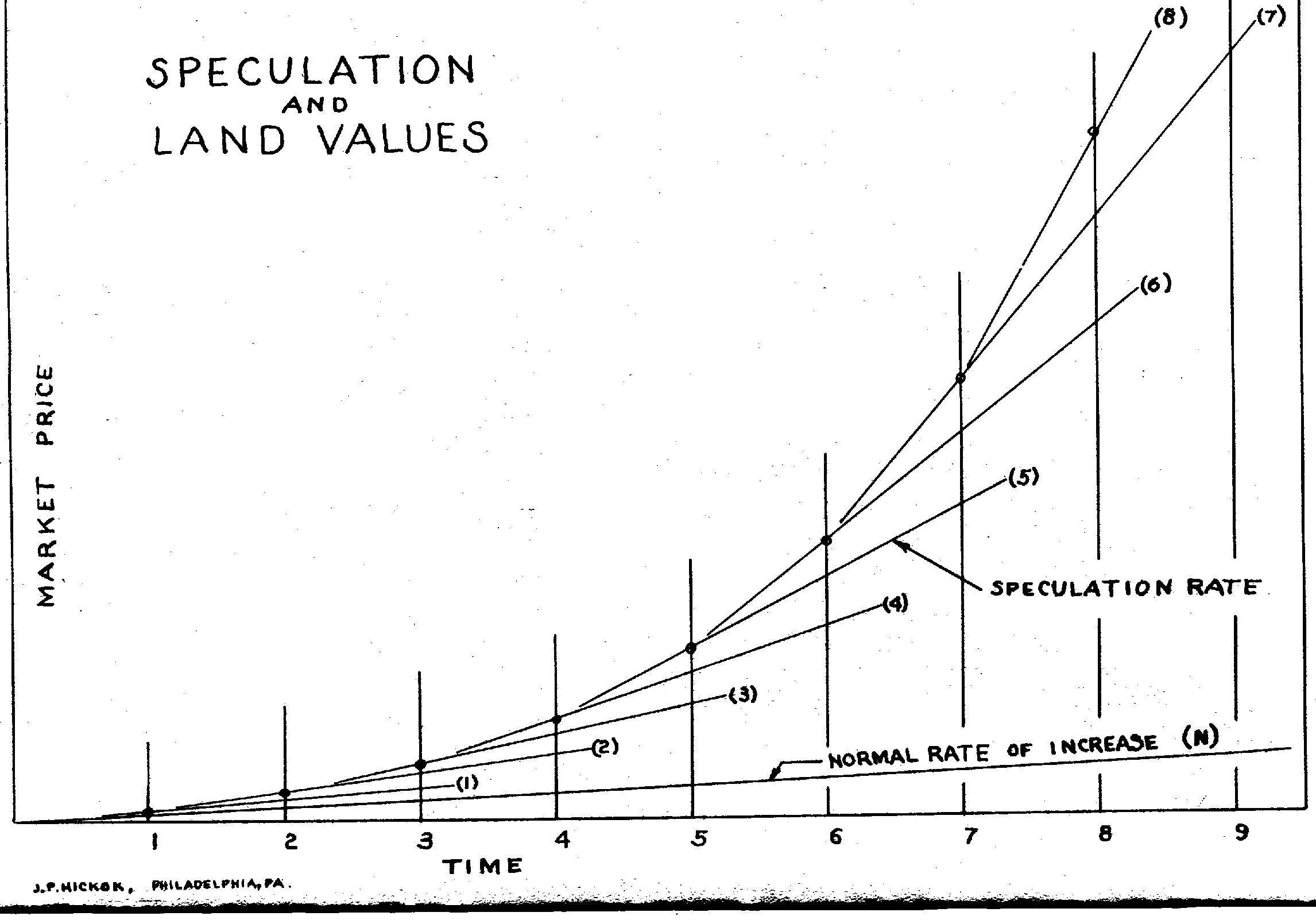

Speculation in land tends to set up chain reactions without any check

on prices. The effect of speculation is illustrated on the

accompanying chart. This comprises a graph, line N, of normal rate of

increase in land values, and graphs, lines (1), (2), (3), etc., of

rates of increases in land prices due to speculation.

Taking a position of time, as at (1), we may have a land owner

willing to sell but wanting to discount as much as possible on future

increases in value, or price. A prospective buyer is willing to pay

more than the actual value at the time, in anticipation of future

increases. The sale is consumated at some price above the true value

as shown by line (N). The difference is an increment of speculation.

Using such transactions as average for the period, there is an

apparent increase in the rate of increases in land values, as shown by

line (1).

Taking another position of time, as at (2), we have another

contingency of seller and buyer, the same as at (1). Thus the selling

price will be above the price designated by line (I), and the rate of

increase will appear to be as shown by line (2). At another position

of time, as at (3), the increment of speculation will then be greater

than that designated by line (2) and the rate of increase will appear

to be that as shown by line (3). With each position of time, as at

positions (4), (5), (6), etc, the apparent rates of increase in land

values will become increasingly greater as shown by lines (4), (5),

(6), etc, respectively, with increasingly greater increments of

speculation. This tends to bring the selling price of land far in

excess of true values, line (N), at the respective positions of time.

It is obvious that as the speculative price of land greatly exceeds

its use value, the buying of land is stimulated not for use but for

future profits. This tends to discourage the use of land and to

encourage the withholding of more and more of land out of use for

future profits, particularly under the realization of extremely high

taxes which would be levied upon any industry applied to it. As

opportunities for employment of labor and capital are thus reduced,

industrial paralysis is sure to follow. When the fever of speculation

has run its course, land held at speculative prices will be forced on

the market, precipitating a rapid decline in all prices, causing

bankruptcy to those caught at the peak and great loss to many who had

inadvertently supported them in the rise in land prices.

The resulting depression will then continue until the damage to the

economy from land speculation has been absorbed. With land prices

reduced to levels justified by increased technology and with

willingness of labor and capital to accept less remuneration, industry

will be normalized and another cycle of land price swings will again

be started. The question is, how many such shocks to our economy can

our civilization endure?

SPECULATION AND LAND VALUES

CONCLUSION

The simple but sure remedy for control of land speculation is

available. Our tax structure should be modified to insure that

increased revenue from land, as such, be taken for public use. We

already tax land values along with building and improvement values. We

have only to establish a policy of increased tax rates on all land

values, actually prices, to control sufficiently the incentive to

speculate in land.*

With the control of the increments of speculation in land, more land

would be readily available for use. Wages to labor and profits to

capital would be increased, repeated shocks to our economy would be

avoided and ultimate collapse of our civilization would be

forestalled.

*APPENDIX

In "Progress and Poverty", Book VIII, Chap. 2, Henry George

writes: "What I, therefore, propose, as the simple yet sovereign

remedy, … is to appropriate rent by taxation."

Whatever procedure must be followed to implement the proposal of

Henry George it must be in form, degree and extent compatible with

popular support. There are two prime factors involved. One is the

assessed valuation of the property and the other is the tax rate.

At the conference of the Henry George School of Social Science in

Montreal, Canada, July 1967, Ted Gwartney, Southfield City Assessor,

told the story of Creative Taxation. This was repeated at the

Conference in Miami Beach, Florida, July, 1968. The Southfield

(Michigan) Plan is to assess all land equitably, irrespective of

improvements, and then to levy upon it the overall real estate tax

rate. This presents a new phase in land value taxation.

Previously, consideration was limited to differential rates of

taxation on land and improvements. To some it is considered more

important, first to lower the rate on improvements and then to

increase the rate on land, to compensate for the loss of tax revenue.

The Pittsburgh Plan, which was designed to stimulate construction, is

an example of this. To others, it is more important, first to increase

the tax rate on all lands and then, out of the increased revenue, to

lower the rate on improvements, providing a net gain in the overall

revenue.

The Southfield Plan is a variation of these procedures. It is based

upon impartial assessment of all land, irrespective of improvements.

This is in effect an increased assessment of vacant or underdeveloped

land, nominally underassessed in many other cities now plagued with

land speculation.

The ultimate goal of land value taxation would involve a long range

program to be worked out, step by step. The Southfield Plan might well

be the first phase in such a program. With popular acceptance of it,

differential rates of taxation might be more readily adopted, pointing

to the ultimate goal of abolition of all taxes save those affecting

the taking of rent for public benefit.

|